Why Does The Sell 1 Buy 2 Strategy Work For HDB Owners

Undeniably, an HDB is an asset.

But is it the best type of property that you can own?

What if there is a way to make use of your HDB to create income-generating assets?

What if this can also be a low-risk way of ensuring you a comfortable retirement?

Okay, I bet you are thinking that this is yet another article asking you to sell your HDB and buy 2 private properties right?

Yes, this is exactly it, BUT, full disclosure, this method is CLEARLY not for everyone. It requires you to fulfil a few criteria before it will work for you.

However, why is this method still so popular among families who can use it?

In this article, let us break down the key reasons why this method is very sound in terms of investment and portfolio planning, and the criteria to employ it.

Reason 1 - Owning 2 potentially high growth assets instead of 1

You have $500,000 and you are given the choice of either:

A) Buying 1 property that is worth $500,000 that grows 2% a year or

B) Buying 2 properties that are worth $1 million and $780,000 respectively that grows 2% a year

Which would you pick?

Your answer will obviously be B.

Effectively, the total outlay that one has to prepare for the purchase of a $1 million property is about $278,000, and $215,800 for the $780,000 property.

These figures include a 25% deposit, Buyer's Stamp Duties and the legal fees to process the transaction.

So, if the value of your HDB is at $500,000 now and provided that you have fully paid down your loan.

You can potentially make use of the HDB to purchase 2 private properties, a total value of $1.78 million, one under the husband's name, the other under the wife's name.

If the property market grows by 2%, you would enjoy $35,600 in capital growth instead of $12,000.

That's almost 3 times the growth.

If you would just hold these 2 properties for the next 30 years, these 2 properties would potentially be worth $3.22m ( at a growth rate of just 2% per year ). The investment property by then will also become a fully passive income-generating asset providing you monthly passive income.

Singapore's property market has proved to be resilient and stable. The government maintains an eagle's watch of the market and will ensure that the growth of the property market is stable and controlled.

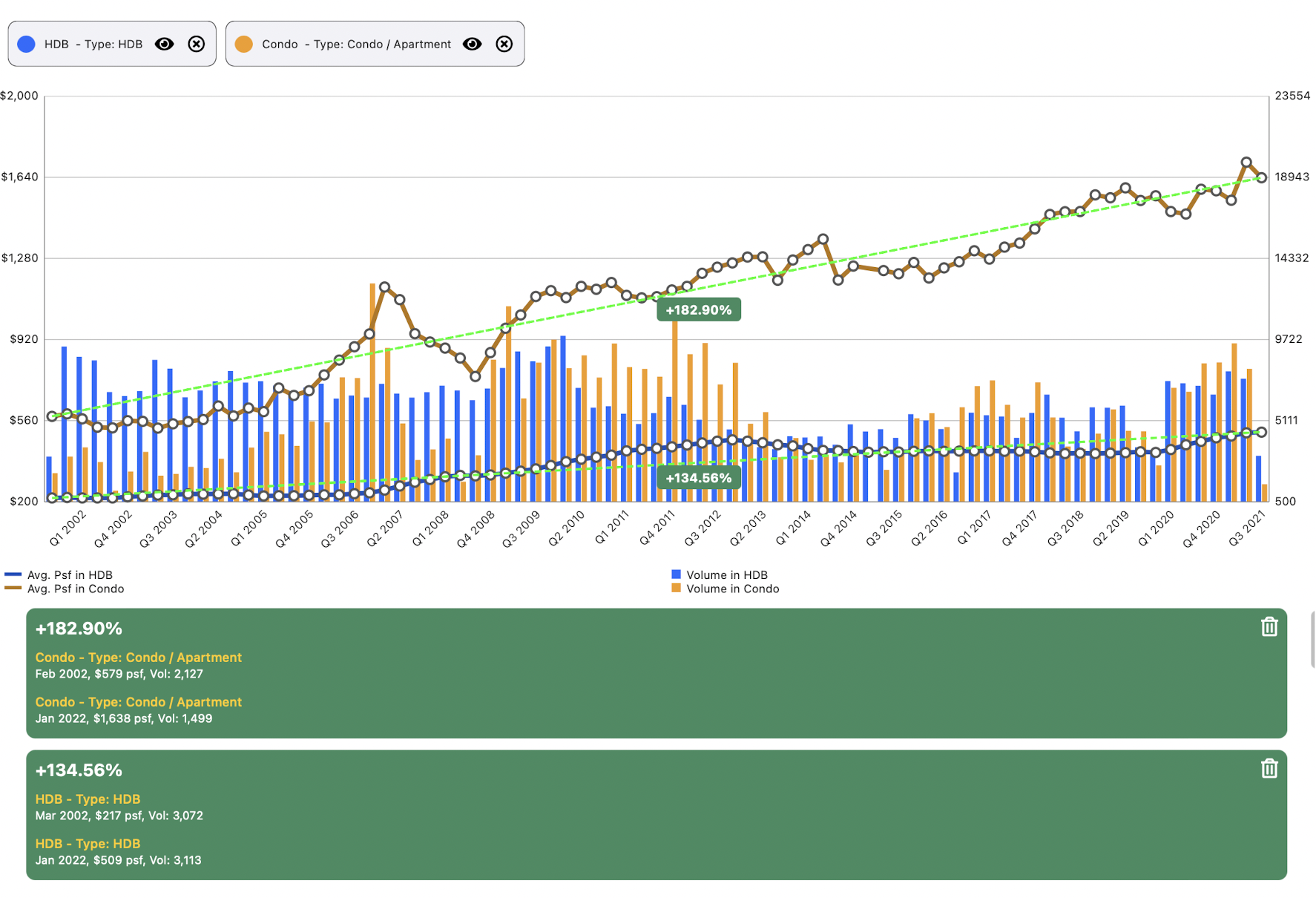

Over the past 20 years, private properties have grown an average of 182%. That's an average of 9.1% annually.

Non-Landed Private Property VS HDB Growth From 2002 - 2022

Along with the stable growth, the Singapore’s property market has low volatility. Even in the midst of the 2008 Financial Crisis, the market took only 2 years to rebound back. Property Investors during that time would still have tenants making the payments for the cost of mortgage for them.

Making properties very suitable as a retirement grade investment.

To pull this off, both the husband and wife have to be working and be earning an average of $6,150 and $4,800 respectively to qualify for the mortgage loans.

But I would have to pay monthly instalments, wouldn't I?

Yes, which brings us to the next reason.

Reason 2 - Having Someone Else Pay For The Cost Of Your Mortgage

Before I go on further, I have to explain what is the cost of your mortgage and why is it different from your monthly instalments.

Your monthly instalment consists of 2 parts, the principal payment and the interest payment.

Monthly Instalments consist of Principal and Interest Payments

The principal payment is part of the value of your property. It adds to the initial deposit that you paid for the property.

Think of it as a bank account, you put money into this property bank account that pays you interest of 2% a year ( or more depending on the growth of the property ).

The interest payment is the actual cost of borrowing from the bank. It goes to the bank and adds no value to your property.

So the actual cost of your mortgage is the interest that you pay to the bank, while the principal payments are made into your property bank account.

Over time, more of the monthly instalments goes into the principal payment ( depositing into your property bank account ), and less into the interest payment.

Now you understand the monthly instalments better, let us move on.

Of the 2 properties, 1 will be used for own stay, while the other will be used to rent out to collect rental income.

The property to be rented out will be able to generate a rental income of $2,275 at a 3.5% rental yield.

( To learn how to pick the right investment properties that generate the highest rental yield, reach out to us here. )

The mortgage instalments of both properties are $4,802, of which $2,002 are interest payments.

This means that your tenant will be paying off the cost of your mortgage, the interest payments, while also depositing $270 a month into your property bank account!

Feeling Of Someone Depositing Money Into Your Bank Account. Naise!

How Nice!

Of the remaining instalments, $2,268 will be paid by CPF from the monthly contribution of each party.

Leaving $259 that has to be paid by cash.

All payments made by you will be made into your property bank account. It is just the same as making monthly payments into a fixed deposit account with a potentially higher interest rate.

If you want your monthly instalments and cost of the mortgage to go even lower, you can stretch the tenure of your mortgage by refinancing the property to a longer tenure, thus lowering your monthly instalments and cost of the mortgage.

You would not need to pay anything in cash.

But wouldn't I have to pay more in interest?

Absolutely not, and here's the reason why.

All properties go through 3 different stages ( except for Freehold Landed Properties )

The 3 stages are the growth stage, stagnation stage and decline stage.

( To learn which stage your property is in now, reach out to me here. )

As a rule of thumb, you need to sell your property just before it hits the stagnation stage and move your funds to another property that is in its growth stage.

Following this rule, you will never end up at the last years of your mortgage payment and pay the extra interest.

Reason 3 - The Advantages of Owning Private Properties

I love HDBs.

They are the foundation of our property market and are what most Singaporeans call home and I am personally very proud of that.

No other countries have achieved what Singapore has done in terms of public housing.

But there are certain advantages to owning private properties in terms of financial flexibility and options.

The ability to sell anytime if required ( SSD applies if sold within 3 years ) vs 5 Year MOP

This gives private property owners a chance to capitalise on any opportunity that arises. Whether it is in the form of another higher potential property or some other form of investment.

The ability to cash out the equity in the value of the property

For a private property owner, when the value of the property rise over the years and the mortgage is being paid down, there is equity that can be withdrawn in the form of an equity loan on the property, without selling the property. HDB owners can only cash out the value of their property by selling it.

The ability to own private properties as a single individual.

Unless you are single and above 35, owning an HDB will require you to be in a family nucleus, along with other criteria. Private properties can be bought as an individual, as a company, even with an unrelated person. Many have used this advantage to own properties with close friends when they could not have done so themselves.

There are other advantages to owning private properties vs HDBs, but I think I will stop here for now.

When functioning as a home, a HDB is as good as any private property, as long as it suits your needs.

But in terms of the financial capability of a property, a private property provides much more options to the homeowner.

I bet you would agree that just these 3 reasons are good enough to warrant the merit of this method and prove why many families are adopting it.

However, as I mentioned at the start of the article, this method is not for everyone and there are criteria to be met

Here they are:

Significant proceeds in CPF and Cash after the sales of HDB

Husband and wife have to have an income that is good enough to support 2 mortgage loans

Affordability ( including funds for safety net )

Skills to select the right property

Significant proceeds in CPF and Cash after the sales of HDB

If your HDB is a BTO flat, chances are that you would have paid down quite a big chunk of your mortgage and the value of your HDB would be quite high, especially during this property market boom.

You can use a sales proceeds calculator to calculate how much you would have in your CPF accounts and cash proceeds if you were to sell your HDB.

This will give you a very good idea of how much you will have to put into your next properties.

Husband and wife have to have an income that is good enough to support 2 mortgage loans

As plain as it is, this strategy will only work for families with both husband and wife working and earning an income that is high enough to get a loan amount that is suitable for each property.

Affordability

The key to affordability is to include a safety buffer in case of any unexpected instances.

Anybody can just lose their jobs or suffer from a setback in their careers.

You would want to be prudent to set aside part of the budget as a fund to support the mortgage payments. This will allow you to recover from the setback and give you time to get back on track with another job.

Never push the purchase price down to the last dime.

Skills to select the right property

Just like any asset, having the skill to pick the right one is the key to making this strategy work.

There is no point in owning 2 properties that do not grow anymore.

There are specific criteria following a set of frameworks that I use to pick properties with the highest growth potential.

The investment property must also be easy to rent out, with a high rental yield and high growth.

These are strict criteria that are non-negotiable to make this strategy work for you.

Conclusion

If you want to find out whether you can adopt this strategy for yourself, book a consultation with me here so that I run through all the criteria with you and make sure that you are in the position to do that.

Even if you are not suitable to use this strategy, I will also evaluate other strategies that best suit you.

Most importantly, you will be able to understand what are the options available for you to make the best possible decision for your property.

You can even prime yourself to own an HDB and a private property at the same time without paying ABSD!